When you switch health plans, one of the biggest surprises isn’t the premium increase-it’s the cost of your generic drugs. You might think all plans cover the same medications the same way, but that’s not true. A generic version of metformin, for example, could cost $3 a month on one plan and $45 on another. The difference? Formulary tiers.

What Are Formulary Tiers and Why Do They Matter?

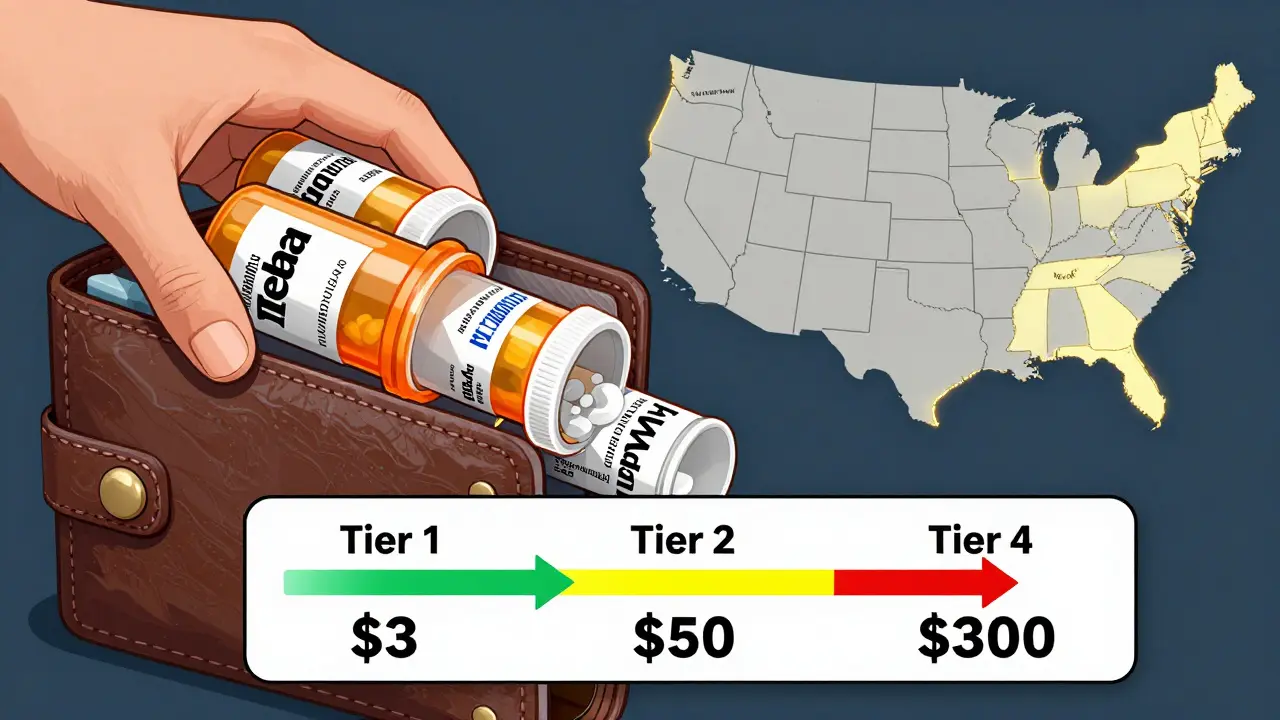

Your health plan’s formulary is just a fancy word for the list of drugs it covers. But it’s not a simple list. It’s divided into tiers, and each tier has a different price tag. The lower the tier, the less you pay. Most plans use a 3- to 5-tier system:- Tier 1: Preferred generics. These are your cheapest options-usually $3 to $20 for a 30-day supply.

- Tier 2: Non-preferred generics or brand-name drugs with generic alternatives. Costs jump to $20-$50.

- Tier 3: Brand-name drugs without generics. Expect $50-$100+.

- Tier 4 and 5: Specialty drugs-often used for chronic conditions like diabetes or rheumatoid arthritis. These can cost hundreds per prescription.

The key? Tier 1 is where you save the most. If your medication is on Tier 1, you’re likely paying a fixed copay, not a percentage of the drug’s cost. That’s huge if you take meds daily.

How Deductibles Change Everything

Here’s where people get tripped up. Not all plans treat prescription costs the same way. Some plans have a separate deductible just for prescriptions. Others combine it with your medical deductible. That means:- If your plan has a combined deductible of $2,000, you’ll pay the full price of your generic drugs until you hit that $2,000 mark.

- If your plan waives the deductible for Tier 1 generics (like Silver Standardized Plans), you pay just $20 per script-even if you haven’t met your deductible yet.

In 2023, Medicare and marketplace plans in states like New York and California started mandating $0 or $3 copays for Tier 1 generics before you meet your deductible. But not every plan does this. If you’re switching from a plan that waives it to one that doesn’t, your monthly cost for a $15 generic could jump to $100+ if you’re still paying toward your deductible.

Medicare vs. Private Plans: Key Differences

If you’re on Medicare, your Part D plan works differently than private insurance.- Medicare Part D (standalone): 2023 base deductible was $505. After that, generics cost $0-$10. But if you hit the coverage gap (the “donut hole”), you pay 25% of the cost.

- Medicare Advantage (MA-PD): These often bundle medical and drug coverage. In 2022, MA-PD plans saved users 18% on average compared to standalone Part D plans-but only if your meds were on preferred tiers.

- Important: Medicare doesn’t require all plans to cover every generic. Some plans drop certain manufacturers. Your levothyroxine might be covered under one brand but not another-even if the active ingredient is identical.

That’s why checking the exact formulation matters. If your plan switches from “Metformin ER 500mg by Teva” to “Metformin ER 500mg by Mylan,” it might move from Tier 1 to Tier 2. You won’t know unless you look.

State Rules Can Make or Break Your Costs

Where you live changes your out-of-pocket costs more than you think.- California: Has an $85 outpatient drug deductible. After that, you pay 20% coinsurance-capped at $250 per script.

- New York: Waives the deductible for generics. You pay a flat $7 copay, no matter what.

- Washington D.C.: $350 separate drug deductible, but caps specialty drug costs at $150.

If you’re moving between states-or even switching plans within the same state-you need to check how your state regulates drug cost-sharing. A plan that looks affordable in Texas might be a nightmare in California.

How to Check Your Medications Before Switching

Don’t guess. Don’t assume. Do this:- Get your current drug list. Include the name, strength (e.g., 500mg), and manufacturer (e.g., “Metformin ER 500mg by Teva”).

- Find the new plan’s formulary. Don’t trust the summary. Download the full PDF. Most insurers have a searchable tool on their website.

- Search each drug by name AND manufacturer. If it’s not listed exactly, assume it’s not covered-or moved to a higher tier.

- Check pharmacy network. Your $3 copay only works if you use a preferred pharmacy. If your local CVS isn’t in-network, you could pay 300% more.

- Use a cost calculator. Medicare.gov’s Plan Finder and Healthcare.gov’s tool let you plug in your drugs and see estimated annual costs. Use them. 37% fewer complaints come from people who do.

People who complete all five steps reduce unexpected drug costs by 73%. That’s not a small number. That’s hundreds-or thousands-of dollars saved.

Common Mistakes People Make

- Thinking all generics are the same. Different manufacturers = different tiers. Your plan might cover “Metformin by Aurobindo” but not “Metformin by Mylan.”

- Ignoring mail-order options. Many plans offer 90-day supplies at lower copays. If you take three meds monthly, switching to mail-order could cut your annual cost by $300.

- Assuming your plan won’t change. Formularies update every January. Even if your drug is covered now, it might be moved next year.

- Not checking insulin and diabetes meds. The Inflation Reduction Act capped insulin at $35/month-but only if it’s on the formulary. If your plan doesn’t include your brand, you’re still paying full price.

What’s Changing in 2025?

The rules are shifting fast:- 2025 Medicare Part D: A $2,000 annual out-of-pocket cap kicks in. But it only applies if your drugs are on the formulary.

- More Silver SPD plans: In 2024, 32 states offer plans that waive deductibles for Tier 1 generics. That number will grow.

- Tier fragmentation: Some plans are splitting generics into Tier 1A (preferred) and Tier 1B (non-preferred). You’ll need to dig deeper than ever.

These changes make it even more important to compare plans carefully-not just by premium, but by what your prescriptions actually cost.

Final Tip: Don’t Wait Until Enrollment

Most people only look at their plan during open enrollment. But if you’re switching mid-year-because you changed jobs, moved, or your plan was canceled-you need to act fast.Call your pharmacist. Ask: “If I switch to Plan X, what will my monthly cost be for these three drugs?” They have access to formularies and can often tell you instantly.

And if you’re on Medicare, use the Medicare Plan Finder before you make any changes. It’s free. It’s accurate. And it’s the only tool that shows you exactly how much you’ll pay for each drug under each plan.

Switching health plans shouldn’t mean switching your meds-or your budget. With the right info, you can save hundreds without changing your treatment.

10 Comments