Ever picked up your generic prescription and been shocked by the price? You thought generics were supposed to be cheap-cheaper than brand names, cheaper than other generics. But suddenly, your levothyroxine or metformin costs $45 instead of $5. You’re not imagining it. And it’s not a mistake. This is how tiered copays work-and why your generic might cost more than you expected.

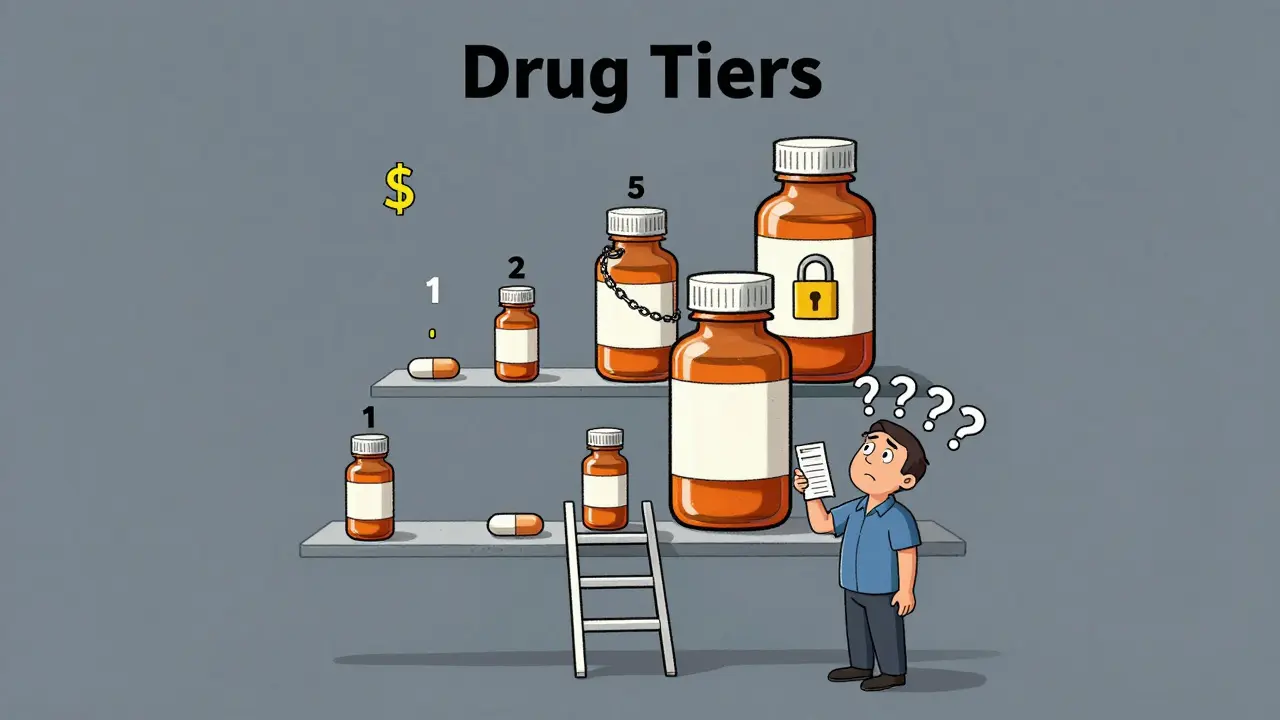

How Tiered Copays Actually Work

Most health plans don’t charge the same amount for every drug. Instead, they sort medications into tiers. Think of it like a pricing ladder. The lower the tier, the less you pay. Tier 1 is usually for the cheapest drugs. Tier 5 is for the most expensive ones, often specialty meds.- Tier 1: Preferred generics. Typically $0-$15 for a 30-day supply.

- Tier 2: Preferred brand-name drugs. Usually $25-$50.

- Tier 3: Non-preferred brand-name drugs. Often $60-$100.

- Tier 4: Preferred specialty drugs. You pay 20-25% of the cost.

- Tier 5: Non-preferred specialty drugs. You pay 30-40%.

Why Your Generic Is in a Higher Tier

You might be thinking: “But it’s the same drug. Why is one generic $5 and another $45?” The answer isn’t about quality, effectiveness, or safety. It’s about money-and who gets it. Pharmacy Benefit Managers (PBMs) like CVS Caremark, Express Scripts, and OptumRx negotiate deals with drug manufacturers. They ask for rebates-discounts paid back to them after the drug is sold. The bigger the rebate, the lower the tier the drug lands in. If your generic is made by Company A and they pay a big rebate to the PBM, it gets placed in Tier 1. If your generic is made by Company B and they don’t pay as much-or any rebate-it gets shoved into Tier 2 or even Tier 3. Same chemical. Same pill. Same doctor’s prescription. But one costs three times more. This isn’t rare. In 2024, Express Scripts moved 87 generic drugs to higher tiers simply because their rebate deals expired. No clinical reason. No safety issue. Just a contract change.

What This Means for You

You might not notice this until you get your bill. You’ve been taking your generic for years. Then one day, your pharmacy says, “Sorry, your usual brand isn’t covered at the low price anymore. We switched you to a different generic.” You didn’t ask for the change. Your doctor didn’t recommend it. But now your monthly cost jumped from $8 to $52. This is called a therapeutic interchange. Pharmacists are often allowed to swap your prescription for a preferred generic without telling you-unless you say no. And if you don’t know your plan’s formulary, you won’t realize what happened until you’re out of pocket. A 2023 survey found that 41% of insured adults ran into this exact problem. And 68% said their insurer gave them no clear explanation. The worst part? It can hurt your health. When people suddenly face a $40 co-pay for a drug they’ve been taking for years, many skip doses or stop taking it entirely. One study showed diabetes patients were 7.3% less likely to stick with their meds when their drug moved to a higher tier.How to Fight Back

You don’t have to accept this. Here’s what you can do:- Check your plan’s formulary-every year, usually in October. Look up your exact drug name and see which tier it’s on. Some plans let you search by drug name on their website.

- Ask your pharmacist: “Is this the preferred generic?” If not, ask if another version is available at a lower tier. Pharmacists often know which ones are cheaper.

- Request a tier exception. If your drug moved up and you’re stable on it, your doctor can submit a form asking the insurer to keep it on the lower tier. Success rate? Around 63%.

- Use GoodRx or SmithRx. These tools show you cash prices and compare copays across tiers. Sometimes paying cash is cheaper than your copay.

- Check for manufacturer coupons. Many drugmakers offer assistance programs. In 2023, these covered 22% of specialty drug costs for eligible patients.

What’s Changing in 2025 and Beyond

Starting in 2025, Medicare Part D will cap out-of-pocket drug spending at $2,000 a year. That’s huge. But it won’t eliminate tiered copays. It just puts a ceiling on what you pay. Some insurers are already adjusting. UnitedHealthcare started putting common generics like atorvastatin and lisinopril into Tier 1 with $0 copays. That’s a win for people on those drugs. But at the same time, they moved less common generics to Tier 2 with $10 copays. The trend isn’t going away. PBMs still control most of the prescription market. And they’re adding more tiers to handle expensive biologic generics-like the copycat versions of Humira or Enbrel. These drugs can cost $5,000-$10,000 a month. Insurers are now putting different versions of them into different tiers, even though they work the same way.What You Should Know

You’re not alone in feeling confused. This system was built to save money for insurers and employers-not to make sense to patients. But that doesn’t mean you’re powerless. Remember: tier placement has nothing to do with how well the drug works. It’s all about rebates, contracts, and profits. Your doctor doesn’t decide your tier. Your pharmacist doesn’t decide it. The PBM does. If your generic suddenly costs more, don’t assume it’s your fault. Don’t assume it’s a mistake. Ask questions. Push back. Use the tools available. And if you’re paying more for the same medicine, you’re not being overcharged-you’re being played by a system designed to hide its true costs. The system isn’t broken. It’s working exactly as intended. But you don’t have to accept it without a fight.Why is my generic drug more expensive than the brand name?

It’s not common, but it happens. Some brand-name drugs are in lower tiers because the manufacturer pays a large rebate to the Pharmacy Benefit Manager (PBM). Meanwhile, your generic may be in a higher tier because its maker didn’t negotiate a good rebate-even though it’s chemically identical. Always check your plan’s formulary to compare.

Can my pharmacist switch my generic without telling me?

Yes, in many cases. This is called a therapeutic interchange. Pharmacies often substitute a preferred generic (lower tier) for the one your doctor prescribed. You’ll only know if you check your receipt or ask. Always say “no substitutions” on your prescription if you want to avoid this.

How do I find out what tier my drug is on?

Log into your insurer’s website and look for the “formulary” or “drug list.” Most plans update this annually in October. You can also call customer service and ask for the tier of your specific drug by name and strength. Third-party tools like GoodRx and SmithRx also show tier info and cash prices.

What’s the difference between preferred and non-preferred generics?

There’s no clinical difference. Both are FDA-approved and contain the same active ingredient. “Preferred” just means the manufacturer pays a bigger rebate to the PBM, so the plan puts it in a lower tier. “Non-preferred” means the rebate is smaller or nonexistent. The drug works the same-you just pay more.

Can I appeal if my drug moves to a higher tier?

Yes. Ask your doctor to submit a tier exception request. They’ll explain why switching drugs could harm your health. If you’re on a stable medication like thyroid or blood pressure drugs, this request is often approved-especially if you’ve been on it for months or years. Success rates are around 63%.

Will the $2,000 Medicare cap fix this problem?

It caps your total spending, but it doesn’t change how drugs are tiered. You’ll still pay more for non-preferred generics until you hit the cap. The system still pushes you toward certain drugs based on rebates, not medical need. The cap helps with affordability, but not transparency or fairness.

Are there cheaper alternatives if my generic is in a high tier?

Sometimes. Ask your pharmacist or doctor if another generic version of the same drug is available in a lower tier. For example, if your lisinopril is in Tier 3, another brand might be in Tier 1. You can also check cash prices on GoodRx-sometimes paying out of pocket is cheaper than your copay.

12 Comments

So the system is designed to screw people over and call it "cost savings"? Cool. I'll just stop taking my meds and save $45 a month. My liver will thank me.

Been there. My levothyroxine jumped from $4 to $42 last year. Called my pharmacy, they said "it's just the new tier." Didn't even ask if I wanted to switch. Feels like being robbed by a spreadsheet.

wait so generics rnt always cheap?? i thought they were just cheap brand names?? lmao i just paid $38 for my metformin and thought i got scammed 😭

You’re not powerless. You’ve got tools. Check your formulary. Ask your pharmacist. Use GoodRx. File a tier exception. This isn’t just about money-it’s about your health. Take control.

Let’s be clear: this isn’t a healthcare system. It’s a rent-seeking oligopoly masquerading as insurance. PBMs are the venal intermediaries who extract value without creating it-like tollbooth operators on the highway of human survival. The drug is the same. The pill is identical. The only variable is the rebate arbitrage. This is capitalism with a stethoscope. And we’re the patients paying for the privilege of being exploited by algorithmic greed. The system doesn’t care if you live or die-it only cares if the rebate check clears.

And don’t get me started on how "preferred" is just corporate-speak for "bribed."

The structural complexity of pharmaceutical benefit management is a global phenomenon, not merely an American anomaly. In India, for example, tiered pricing exists under different regulatory frameworks, yet the underlying economic incentives remain similar. Transparency remains the critical gap across jurisdictions.

Thank you for this detailed breakdown. I’ve seen this happen to my mother-she didn’t understand why her blood pressure medication suddenly cost $50, and her doctor didn’t know either. It’s heartbreaking. Everyone should be required to check their formulary annually. It’s not just a suggestion-it’s a necessity.

so like… my generic lisinopril went from $0 to $20?? 😭 i didn’t even get a text. no warning. no notice. just my card getting declined at the pharmacy like i’m some kind of criminal?? 🤡 #pharmacybetrayal

People still act surprised when the system screws them? Wake up. This has been the plan since 2010. PBMs are the real villains. Doctors are just pawns. Pharmacies? They’re just cashiers. You think your insurance cares about your health? They care about their quarterly earnings. You’re a line item. Not a person.

63% success rate on tier exceptions? That’s not a fix. That’s a placebo. You’re still fighting a rigged system. The real solution is eliminating PBMs entirely.

They’re not just moving drugs-they’re moving lives. My friend skipped her insulin for three months because of this. She ended up in the ER. Then the bill came. $22,000. The PBM made $400 in rebates. Who won? Not her. Not you. Not us.

I just checked my formulary and my generic was moved to tier 3. I didn’t even know they could do that. I’m gonna call my doctor tomorrow. Maybe they can help. I’m tired of feeling like a pawn.